Does the President Matter…

A lot has been made about the recent election and the “economy.” If you turn on the news,

whether it was TikTok, Facebook, opening up the newspaper (yeah, like anyone does that

anymore) or going to your favorite cable news channel, you’re going to hear about the

“economy,” inflation, rate cuts, tariffs, etc… Maybe you’re excited about the coming

administration or have anxiety about the coming administration. In the end you should know

that the administration, any administration, shouldn’t be taking credit for the economy or blame,

at least not fully. There are always things that can be done to influence the “economy” by an

administration, but in the end like time, the economy marches on.

So, why is “economy” in quotes here? That’s because it means something different to every

individual. According to the Journal of Economic Perspectives, Vol. 30, No. 1, Winter 2016 (in

case you’re really bored…) the word economy comes from two Greek words oikos and nemein.

And, at first, I thought of yogurt…. But Oikos means “Household” and Nemein means

“Management.” It is generally a description of the production and consumption of goods and

services of a region. The ancient Greeks, as in so many other ways, had a good take on this.

The economy is about the household. Some households will think it good; others will think it

bad.

Your clients who are going through a divorce or trying to recover from an injury are going to be

worried about their household first and foremost. The issue in our polarized society is that they

are either going to be overly optimistic or overly anxious. Daily ups and downs will seem like a

bellwether or omen of future results. Reports on consumer confidence, trade imbalances,

suggestions from TV stars from bygone days to buy Gold, or Reddit users suggesting meme

stocks can all add to the noise they’re experiencing.

In order to quiet the noise in my head, I did some digging… not too much because I want to

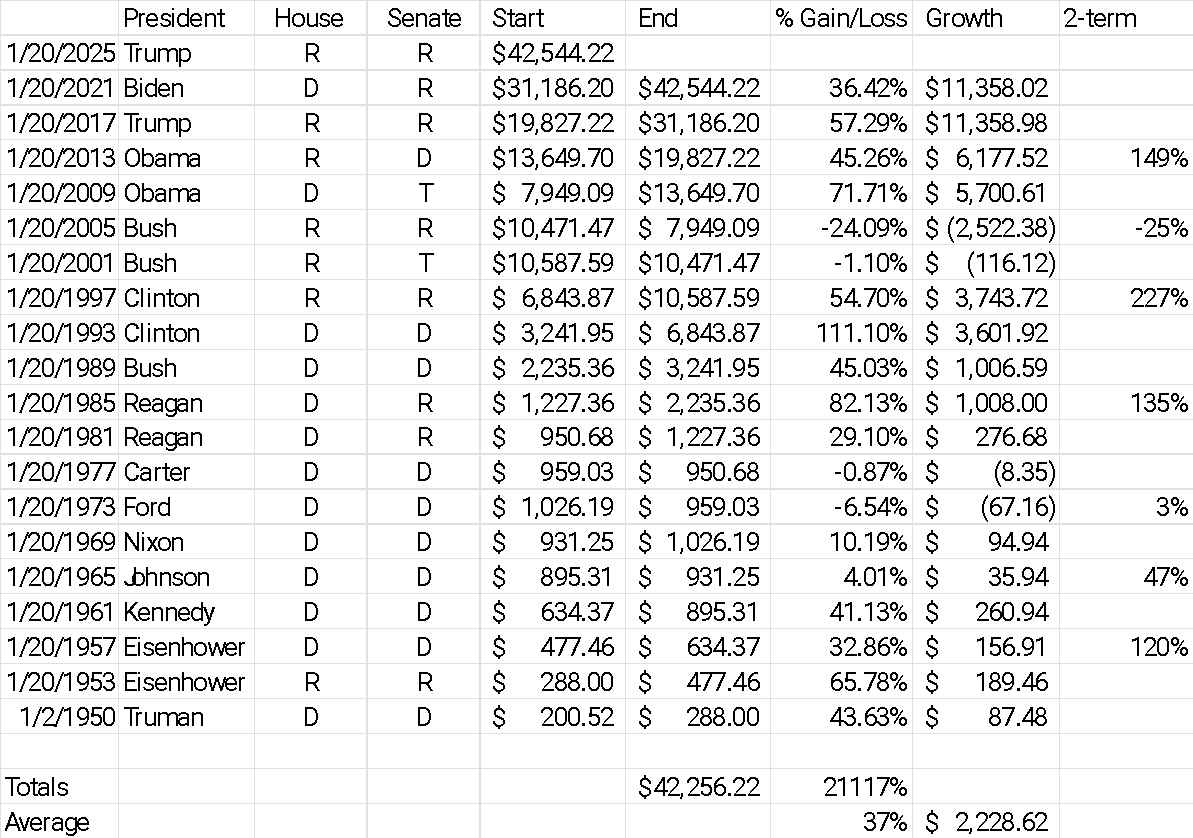

keep these short, but just enough to show you it will all be okay. I used the Dow Jones

Industrial Average on or immediately before inauguration day going back to January 2, 1950 (I

know that’s not inauguration day, but it is when Statmuse had its earliest value for the DJI. I

could have done this back to 1881 using Wikipedia’s data, but that seems a bit much since most

of us don’t even remember 1950. I also know that the DJIA is not the “economy,” but it has

been widely recognized as a symbol of the health of the American economy, and most people,

whether they know it or not have some investment in this standard. And, as mentioned above, it

can be run back to before Lincoln’s assassination.

Since 1950 there have been 19 terms (yeah that’s 76 years), there have been 14 different

presidents, 38 different iterations of congress, hot and cold wars, pandemics, recessions, crisis,

terrorist attacks, some assassinations, a few assassination attempts, mass migrations,

environmental disasters, booms, busts, strikes, plane crashes, military actions, passed and

failed constitutional amendments, and just about anything Billy Joel could have thrown into a

song. With all that run-on sentence being read here are 10 other fun facts.

- Since January 2, 1950, the DJIA is up 21,117%.

- The average gain over the course of an administration is 36.72%

- The largest % loss was 24.09% by Bush parte deux in his second term. This is an

outlier as the other losses by presidents over the course of their term did not exceed 7%. - Both parties have had presidencies with loss over the course of their term.

- The largest gain was by Clinton in his first term at 111% followed by Reagan at 82% then

Obama at 71%, Eisenhower at 66%, and Trump 1 at 57% - By percentage, the largest single day decline was Black Monday, Oct. 19,1987, falling

22% to 1,738.74. The market still finished Reagan’s second term up 82% from 1985 to

1989 despite the crash. - The largest point drop was March 16, 2020, remember COVID, when the DJIA lost 2,997

points, 12.9%. The largest gain was on March 24, 2020, when it gained 2,113. - Clinton, Obama, Reagan, and Eisenhower are standouts in the “two-term” category.

Kennedy (using Johnson’s terms) netted a 47% growth over 8 years and Nixon/Ford

netted a paltry 3%. Only Bush II had a significantly depressed result at -25% over two

years. - Running this on the first trading day of 2025 with the DJIA at 42,544.22 puts Trump 1

and Biden both at $11,358 in gains. The difference is 57% to 36% growth respectively

because of the starting value. - The average increase in value has been $2,228.62 dollars over the last 19 terms, yet

only 6 terms have recorded increases in excess of that number. All 6 have occurred

since 1993.

I put my spreadsheet below. Please feel free to check my work. Always happy to acknowledge

an error. That being said. If your client is looking for some help with the anxiety caused by the

new administration, this should let you know that even in the worst eight years of the last 75, we

came out okay and in the best, we crushed it. Sharp drops are usually made up for with

significant gains in short order. Clients who have too much of one thing or another may feel a

pinch. Getting professionals involved who can help with the conversations surrounding money

is going to make your and your clients’ lives better… If you need help having these

conversations, please look us up.